Collection Letter Template

Welcome to the world of debt collection and the power of effective communication! In this article, we will delve into the art of collection letters and how they can be your ally in recovering outstanding debts. Whether you're a small business owner or a seasoned entrepreneur, understanding the ins and outs of collection letters is essential for maintaining healthy cash flow and fostering professional relationships.

In this comprehensive guide, we will cover everything you need to know about collection letters and provide you with valuable insights to help you navigate the debt collection process with finesse. We'll explore the key elements to include in a collection letter, step-by-step instructions on crafting a persuasive letter, and what to do after the letter has been sent. We'll also discuss the importance of adhering to legal considerations to ensure compliance with debt collection laws.

Table of Contents

.webp)

If you are looking for other templates or a general introduction to the concept of demand letters, please have a look at our demand-letter guide.

What is a Friendly Collection Collection Letter?

Alright, let’s dive right in! When you’re running a business, cash flow is king. So, it can be a real bummer when a client or customer isn’t coughing up what they owe you. This is where a collection letter comes into play. But what exactly is a collection letter? Well, my friend, you’re in the right place to find out.

A debt collection letter reminds a nonpaying client of their debt to you or warns of near-future legal action.

In its simplest form, a collection letter is a gentle nudge (or sometimes a firmer push) to remind someone they need to pay up. It’s that polite (and later, more insistent) note saying, “Hey, you owe some money, and it’s time to settle the score.” It’s typically sent when a bill is overdue, and the usual invoices and reminders haven’t got the job done.

But here’s the kicker: a collection letter is not just about saying, “Give me my money.” It’s also an essential tool in maintaining a professional relationship with the debtor. You see, you don’t want to scare them off or burn any bridges. You want to encourage them to clear the debt so that you both can carry on with business as usual.

Now, don’t get mixed up between collection letters and collection agency letters. The latter is from a third-party agency that specializes in collecting debts, and they usually step in when your own efforts haven’t borne fruit. A collection letter, on the other hand, is something you send before things get that far. It’s your way of giving the debtor a chance to make things right before the big guns come out.

Also, it’s important to note that collection letters often come in stages. The first letter is usually like a friendly tap on the shoulder, while subsequent letters turn up the heat a little bit more each time. This way, you’re progressively asserting the seriousness of the situation, without coming out of the gates too strong.

In essence, a collection letter is an attempt to collect the money that’s owed to your business in a professional and systematic manner. It’s a fine balance between persistence and politeness – with the end goal of getting that cash flowing back into your business.

Now that you’ve got the gist of what a collection letter is, let’s move on to some essential considerations before you start drafting one. Stick around!

When to hire a debt collection agency

Once you've gone through the debt collection steps, it's time to consider bringing in the big guns in the form of a debt collection agency like Debitura. We work for businesses of all sizes and have negotiation experts who can handle the difficult business of debt collection on your behalf. Alternatively, you could start working with us before the stresses of debt collection start to create that stomach ulcer you've been trying to avoid.

Remember that cash flow problems are one of the biggest reasons for businesses to fail - don't let that be you!

Different types of debt collection letters

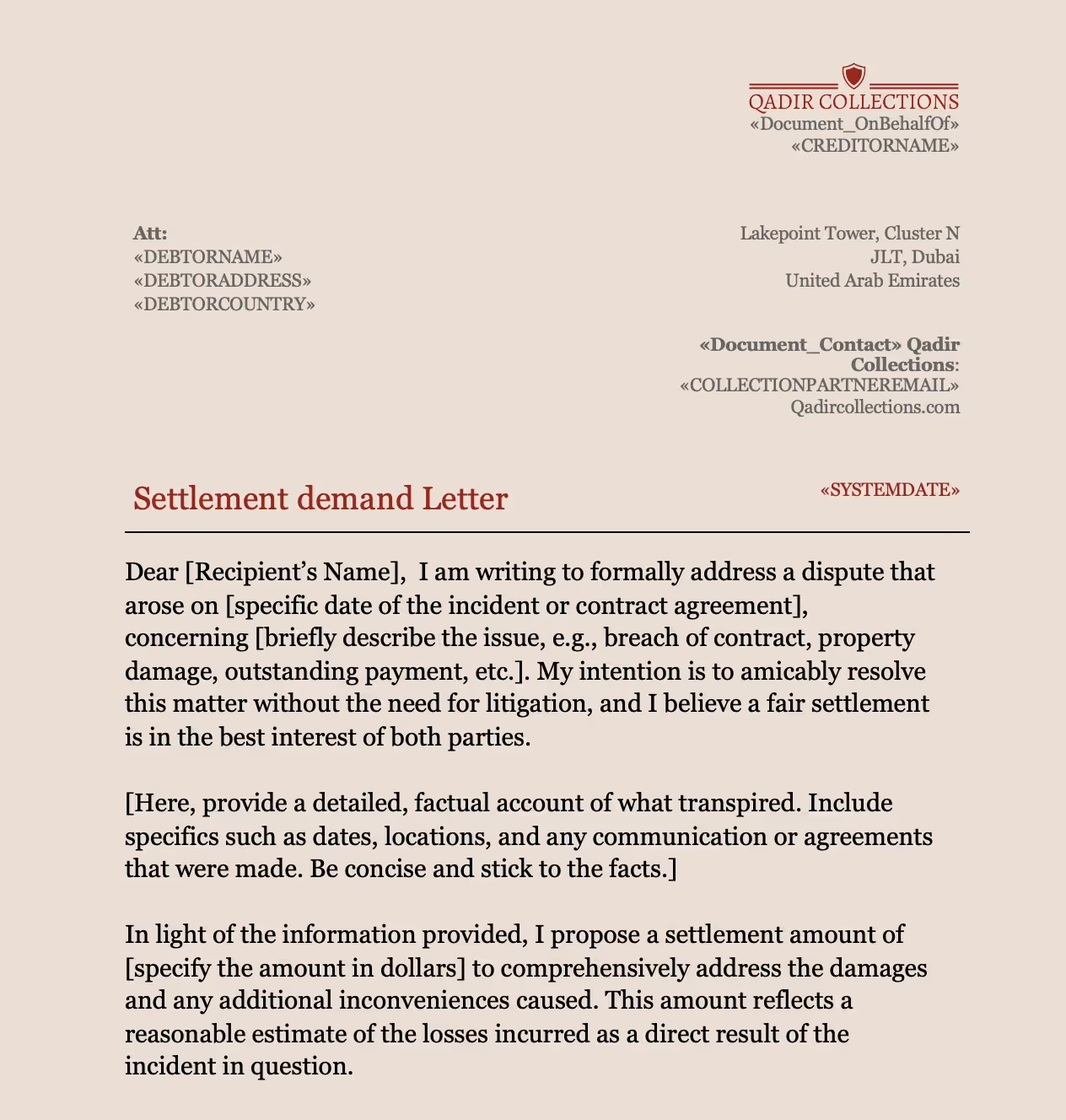

Below, we outline a typical dunning process, involving a series of 6 progressively firmer reminders, culminating in the involvement of a debt collection agency. This process takes a graduated approach, starting with a friendly reminder and gradually increasing in seriousness. It gives the debtor ample opportunity to resolve the issue before it is escalated to a collection agency. Keep in mind that local regulations and best practices for debt collection can vary, so it's a good idea to ensure that your process complies with applicable laws.

- Initial Friendly Reminder (Day 1 after due date): Send a friendly reminder email or letter to the customer, kindly mentioning that the payment is now past due and requesting them to settle the invoice as soon as possible.

- First Payment Reminder Letter (Day 7 after due date): Send a more formal reminder letter that includes details of the invoice, such as invoice number, due date, and the amount due. This letter should still maintain a polite tone, but be firmer than the initial friendly reminder.

- Second Payment Reminder Letter (Day 14 after due date): Send a second reminder letter, reiterating the details of the invoice and expressing the urgency of the matter. Mention that failure to resolve the issue might result in further action.

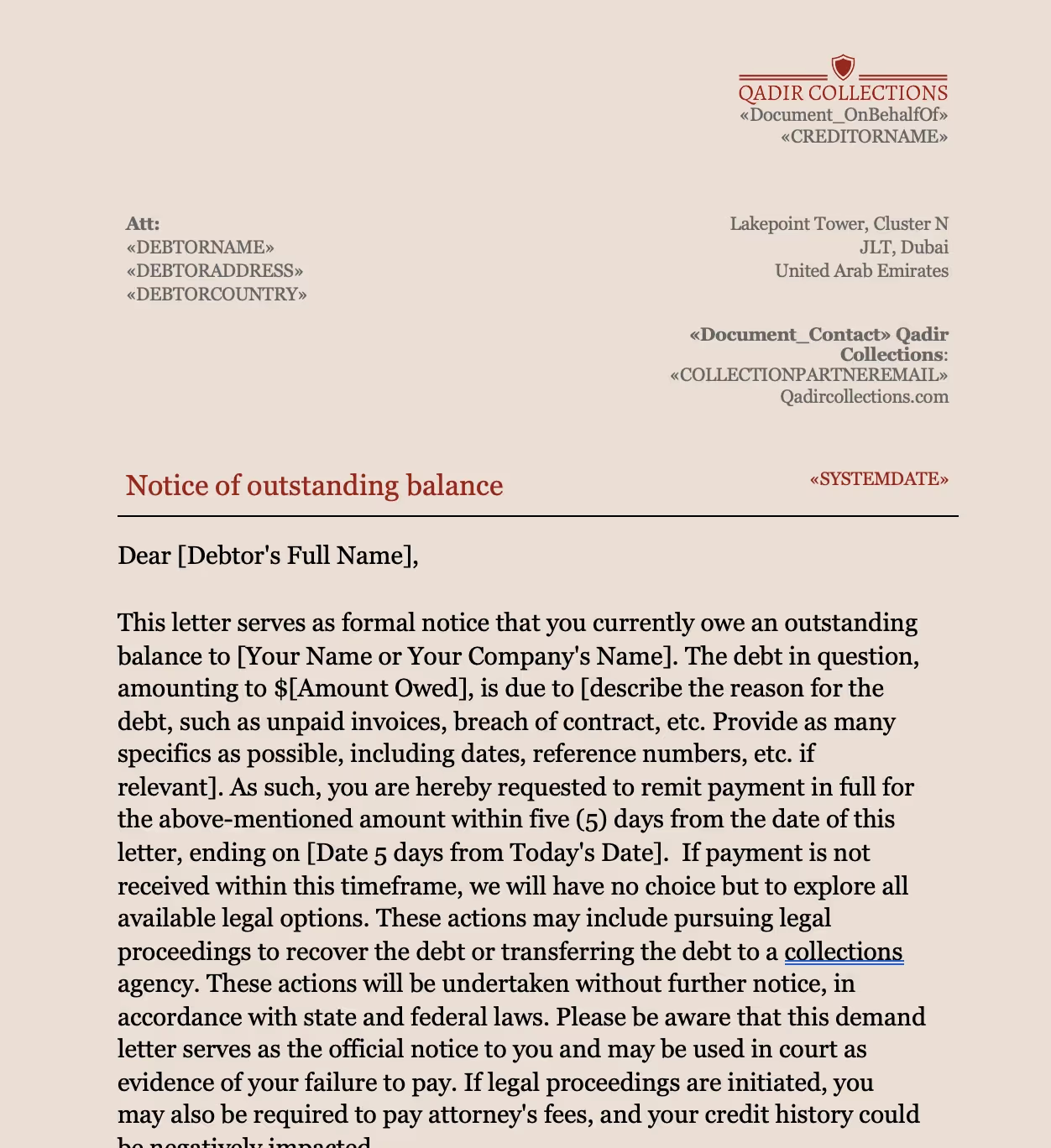

- Final Notice Letter (Day 21 after due date): In this letter, be firm and clear that this is the final notice before escalating the matter. Mention the possibility of involving a debt collection agency or pursuing legal action if the payment is not made by a specific date.

- Notice of Handover to Collection Agency (Day 30 after due date): Send a letter informing the debtor that since they have not responded or made payment, the debt has been passed on to a collection agency. This should be sent immediately before passing the account to the agency.

- Collection Agency Letter (Day 35 after due date): This letter is sent by the collection agency. It will notify the debtor that the debt has been handed over to them, and they are now handling the collection. It should state the debtor’s rights and what steps will be taken if the debt remains unpaid.

Need a different format? Browse all demand letter templates.

Free Collection Letter Templates

Navigating the delicate waters of debt collection requires tact, persistence, and clear communication. To assist you in this endeavor, we have meticulously crafted a series of reminder templates that guide you through various stages, from gentle nudges to the final handover to a collection agency.

Please be advised that the templates provided herein serve as general examples to streamline the payment reminder process. The actual content, information, and phrasing should be adapted based on your specific situation, company policies, and the legal jurisdiction in which you operate. Different locations may have distinct laws and regulations regarding debt collection, and it is vital to ensure that your communications are compliant with these regulations.

Utilizing these templates can save time and effort, and provide a structured approach to communicating with customers who have outstanding payments. However, remember to maintain the balance between being firm in your request for payment while preserving the valuable relationship you have with your clients.

Feel free to customize these templates to reflect your company's voice and values, and ensure they align with the legal requirements of your area.

Collection Letter Template

Initial Friendly Collection Letter Sample (Day 1 after due date):

Subject: Friendly Reminder: Invoice #[Invoice Number]

Body:

Hi [Recipient Name],

I hope this message finds you well. Thank you for being a valued customer. We truly appreciate your business and the relationship we’ve built together.

As our accounting team was going through the records, we noticed that the payment for Invoice #[Invoice Number], which was due on [Original Due Date], is still pending. We understand that sometimes payments can be overlooked in the hustle and bustle of everyday business.

For the continuity of our smooth collaboration, could you kindly review the payment status and, if not yet done, process the payment at your earliest convenience?

We appreciate your prompt attention to this matter. Please feel free to reach out if there are any issues or queries regarding the invoice. We're here to help!

Wishing you a great day ahead.

Warm regards,

[Your Name]

[Your Position]

[Your Company]

This template is friendly and courteous, and it reminds the customer of the past due invoice without being too forceful. It's designed to maintain a positive relationship with the customer while nudging them to take action regarding the payment.

First Payment Reminder Letter (Day 7 after due date)

Subject: [Your Company’s Name] Invoice #[Invoice Reference Number] Payment Reminder

Body:

Hi [Recipient's First Name],

I hope this email finds you in good health and high spirits.

I wanted to gently follow up regarding the payment of [Amount Owed on Invoice] pertaining to our Invoice #[Invoice Reference Number], which was due on [Date Due]. As of now, we have not received the payment.

Understanding the myriad of responsibilities we all juggle, it’s possible this invoice slipped through the cracks. As this payment is essential for our financial processing, I would greatly appreciate it if you could let me know when we can expect the payment to be settled.

For your convenience, I have attached a copy of the invoice.

Thank you so much for your prompt attention to this matter. Please don’t hesitate to reach out if there are any issues or if you have any questions.

Warm regards,

[Sender's First Name]

[Sender’s Position]

[Your Company’s Name]

This template is still polite and slightly more formal, emphasizing the importance of the payment while being considerate of the recipient. It serves as a reminder without straining the business relationship.

Second Payment Reminder Letter (Day 14 after due date):

Subject: Urgent: Outstanding Invoice #[Invoice Reference Number] - Immediate Action Required

Body:

Dear [Recipient's First Name],

I hope this message finds you well.

As part of our financial records review, we have observed that there is still an outstanding balance of [Amount Owed on Invoice] for Invoice #[Invoice Reference Number], which was due for payment on [Date Due]. This is our second reminder regarding this payment.

We understand that there might be various reasons for the delay, but it is imperative for the continuity of our services and business relationship that this invoice is settled as soon as possible.

Please be advised that if the payment is not received within the next 5 business days, we may have to take further action to collect the amount due, which could include late fees or involvement of a collection service.

We urge you to address this as a matter of priority. If there is a specific issue preventing the payment, or if you require any clarification regarding the invoice, please do not hesitate to get in touch with us.

Attached is a copy of the invoice for your reference.

Thank you for your immediate attention to this matter.

Sincerely,

[Sender's Full Name]

[Sender's Position]

[Your Company's Name]

[Contact Information]

This template is firmer and expresses the urgency of the matter, indicating that the issue needs to be resolved immediately to avoid further action. It’s important to maintain professionalism while making the seriousness of the situation clear.

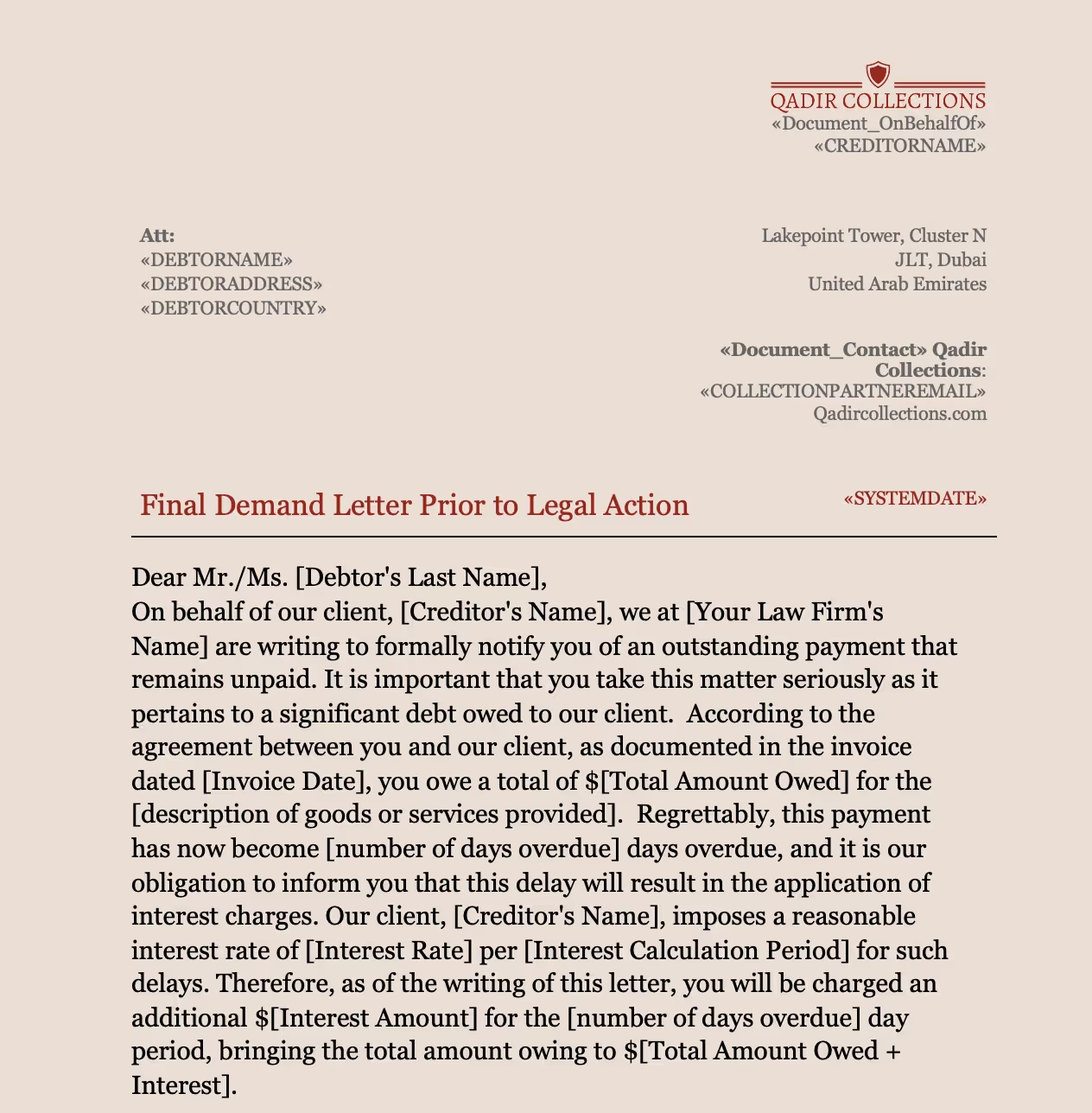

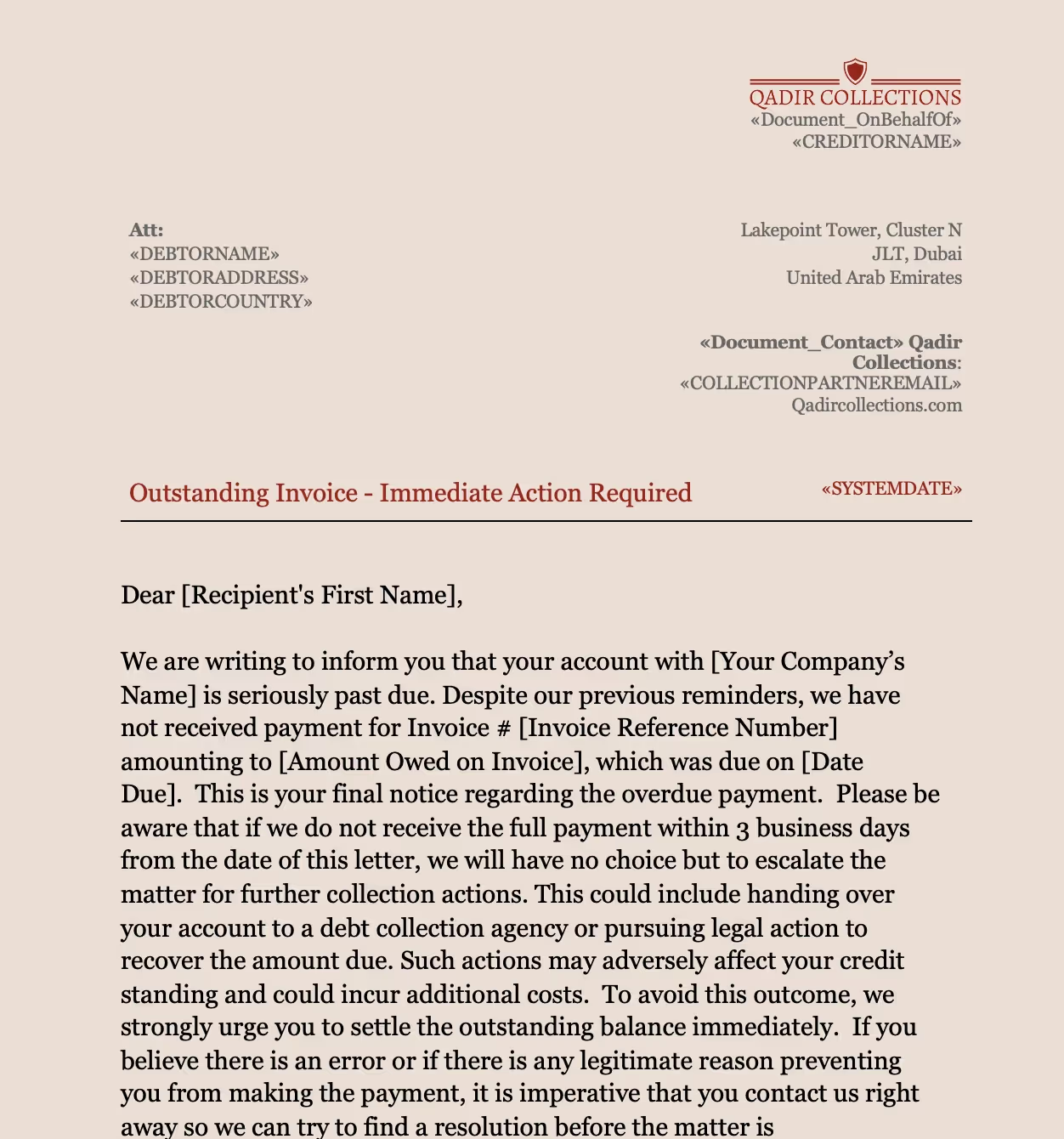

Final Notice Letter (Day 21 after due date):

Subject: FINAL NOTICE: Immediate Payment Required for Invoice #[Invoice Reference Number]

Body:

Dear [Recipient's First Name],

We are writing to inform you that your account with [Your Company’s Name] is seriously past due. Despite our previous reminders, we have not received payment for Invoice #[Invoice Reference Number] amounting to [Amount Owed on Invoice], which was due on [Date Due].

This is your final notice regarding the overdue payment.

Please be aware that if we do not receive the full payment within 3 business days from the date of this letter, we will have no choice but to escalate the matter for further collection actions. This could include handing over your account to a debt collection agency or pursuing legal action to recover the amount due. Such actions may adversely affect your credit standing and could incur additional costs.

To avoid this outcome, we strongly urge you to settle the outstanding balance immediately.

If you believe there is an error or if there is any legitimate reason preventing you from making the payment, it is imperative that you contact us right away so we can try to find a resolution before the matter is escalated.

Attached is a copy of the invoice for your records.

We hope it does not come to that, and we can conclude this matter amicably. Thank you for your prompt attention to this serious issue.

Sincerely,

[Sender's Full Name]

[Sender's Position]

[Your Company’s Name]

[Contact Information]

This letter is much more firm and direct, making it very clear that this is the final opportunity for the customer to resolve the payment issue before it is escalated to a more serious collection action.

Notice of Handover to Collection Agency (Day 30 after due date):

Subject: Important: Account Handover to Collection Agency - Invoice #[Invoice Reference Number]

Body:

Dear [Recipient's First Name],

I am writing to inform you that despite our repeated attempts to communicate with you regarding the unpaid invoice #[Invoice Reference Number], dated [Date Due], and totaling [Amount Owed on Invoice], we have not received payment or any communication regarding this matter.

As a result, we have exhausted the options available to us for internal collections. Your account has now been referred to a debt collection agency, effective immediately. This agency will now be responsible for collecting the outstanding debt on our behalf.

Please be advised that having this debt with a collection agency could have a negative impact on your credit score and could make it difficult for you to obtain credit in the future.

It’s also important to note that additional fees and charges might accrue as part of the debt collection process, which will be your responsibility.

If you wish to avoid further actions and additional costs, it is crucial that you contact the collection agency promptly and make arrangements with them to settle the outstanding debt.

For your records, the contact details of the debt collection agency are:

[Collection Agency Name]

[Collection Agency Address]

[Collection Agency Phone Number]

[Collection Agency Email Address]

We sincerely hoped that it would not have come to this, and we regret any inconvenience this might cause.

Thank you for your attention to this matter.

Sincerely,

[Sender's Full Name]

[Sender's Position]

[Your Company’s Name]

[Contact Information]

This letter is very direct and formal, indicating that the debt has been passed on to a collection agency and outlining the potential consequences for the debtor. It advises the debtor to contact the collection agency to resolve the outstanding debt.

Collection Agency Letter (Day 35 after due date):

Subject: Notice of Debt Collection: Invoice #[Invoice Reference Number]

Body:

[Recipient's Full Name]

[Recipient's Address]

[Date]

Dear [Recipient's First Name],

This letter is to inform you that your account with [Original Creditor's Name] related to Invoice #[Invoice Reference Number] dated [Date Due], totaling [Amount Owed on Invoice], has been placed with our agency, [Collection Agency Name], for collection.

As of the date of this letter, the current outstanding balance is [Amount Owed, including any additional fees].

Please be aware that this is an attempt to collect a debt, and any information obtained will be used for that purpose. You have the right to dispute the validity of this debt within 30 days of receiving this notice. If you do not dispute the validity of the debt or any portion thereof within this period, we will assume the debt to be valid.

In the event you do dispute the debt, or any portion thereof, within the 30-day period, we will obtain verification of the debt and mail you a copy of such verification.

We urge you to resolve this debt promptly to avoid any further action, which could include reporting the debt to credit bureaus or pursuing legal action.

You may remit payment to:

[Collection Agency Name]

[Collection Agency Address]

Please include the reference: Invoice #[Invoice Reference Number] with your payment.

If you have questions or wish to discuss payment arrangements, please contact our office at [Collection Agency Phone Number].

Your prompt attention to this serious matter is strongly advised.

Sincerely,

[Agent's Full Name]

[Collection Agency Name]

[Contact Information]

Please note that this letter includes elements that are often required by law in many jurisdictions, such as the right to dispute the debt. Regulations surrounding debt collection can vary by location, so it's important to ensure that the letter complies with the applicable laws in the jurisdiction where it's being sent.

Note: This is a general example of a demand for payment letter. The actual information and phrasing should be adapted based on your specific situation and legal counsel, as applicable. This information does not constitute legal advice and it is always best to consult with a legal professional in your area for tailored guidance.

Are you looking for other demand letter templates?

Klik here to browse our full library.

What Should You Consider Before Sending a Collection Letter?

Hold your horses! Before you whip out your pen and paper (or more likely, open up your email) to get that collection letter out the door, there are a few things you need to take into account. Think of this as the prep work – it’s not the most glamorous part, but boy, is it important.

- Importance of Understanding the Debtor's Situation: Empathy is key. You don't want to be that person who sends a stern collection letter to someone going through a rough patch. Maybe their business hit a bump or they’re facing some personal issues. Understanding the debtor’s situation can help you craft a letter that’s firm, but fair. A little compassion can go a long way in maintaining a positive business relationship.

- Consideration of the Business Relationship with the Debtor: Speaking of relationships, let’s talk about how vital it is to consider your history with the debtor. Is this a one-time customer or a long-standing client? Are they typically good for it? The nature of your relationship can help inform the tone of your letter. A valued client might deserve a more lenient approach, while a habitual late-payer might need a firmer nudge.

- Timing for Sending a Collection Letter: They say timing is everything, and when it comes to collection letters, they’re not wrong. Send it too early, and you might come off as impatient; too late, and you might be in a cash flow pickle. The trick is to send the letter once the payment is overdue, but not so late that it gets buried in a pile of other forgotten responsibilities. A good rule of thumb is to send the first letter within a week after the payment was due.

- Importance of Adhering to Laws and Regulations (Fair Debt Collection Practices Act): Now, let’s get serious for a moment. Sending a collection letter isn’t just about what you want to say, it’s also about what you need to say and how you should say it. The Fair Debt Collection Practices Act (FDCPA) has a whole set of rules about how you can communicate with debtors. Trust us, you don’t want to tangle with legal troubles. Make sure you’re informed about and comply with these regulations. If you’re unsure, it’s not a bad idea to get some legal advice.

Alright, now that we’ve got the considerations out of the way, you’re in a better position to start penning that letter. But wait, what about the costs involved? Stick around as we get into the nitty-gritty of the potential costs of drafting and sending a collection letter.

What is the Cost of Drafting and Sending a Collection Letter?

Alright, let’s talk money. You’re here to collect debts, not to spend more, right? But as the saying goes, “You’ve got to spend money to make money.” Sending a collection letter isn’t without its costs. Here’s the 411 on what you might be looking at in terms of expenses. Lets break it down:

- Drafting: Depending on how savvy you are with words, you might be able to whip up the letter yourself. But if writing isn’t your forte, hiring a professional writer or using a great collection letter template could be the ticket. These options might cost you anywhere from a few bucks for a template to a bit more for a pro writer. You can download our free templates in this article to get started for free.

- Legal Review: Don’t play around with this one. Making sure your letter is on the up-and-up legally is crucial. Consulting a lawyer to review your letter for compliance with the Fair Debt Collection Practices Act and other laws could range from $100 to $300. You can also use our compliant templates for free.

- Mailing: You could send your letter via email (pretty much free, except for your internet bill), but sometimes a good old-fashioned paper letter carries more weight. Factor in the cost of printing and postage, which might not be much but is worth considering.

Now, let’s get to the fun part – the ROI, or return on investment. Sending a collection letter might have its costs, but it could also mean recovering money that might otherwise be lost. Depending on the size of the debt, even after the costs of drafting, reviewing, and sending the letter, you could be looking at a nice chunk of change making its way back to your business.

Consider this: if not sending the letter means not getting paid at all, then even with the expenses, it’s still a win if you manage to collect.

So, when you’re weighing the costs, think about the potential gains. It’s not just about spending money; it’s about strategically investing it to recover what’s owed to you.

Phew! We’ve talked numbers, and your wallet might be feeling lighter just thinking about it. But wait, what are the upsides of going through all this? Up next, we’ll dive into the advantages of sending a collection letter. Stay tuned!

Debitura is not a law firm or debt collection agency. Instead, we are a platform that connects you with vetted local collection agencies and lawyers worldwide. Leverage our network of 500+ local collection agencies and lawyers across 183 markets for effective, on-the-ground debt recovery.

•Hand-picked Agencies: We connect you with the best debt collection agencies and law firms worldwide.

•Performance-Based Selection: Our partners are constantly tested and evaluated to ensure top performance.

•Access to the Best: Only the best-performing agencies remain in our network, giving you access to superior debt recovery services regardless of where your debtors are.

.svg)

Simplify your legal framework with our 'No Cure, No Pay' standardized agreement across all local partners. Ensuring convenience for international creditors, we offer a standard debt collection agreement across jurisdictions and local partners.

•No Cure, No Pay: Enjoy risk-free pre-legal debt collection with no upfront costs.

•Standardized Pre-legal Agreement: Our partners adhere to a transparent and standardized debt collection agreement, streamlining your legal framework across jurisdictions and partners.

•Competitive Legal Rates: For legal interventions (lawsuits, debt enforcement, insolvency proceedings, etc.), receive up to 3 competitive quotes from our network of local attorneys.

Explore our pricing

Quick, professional and hassle-free B2B and B2C debt collection. 87% Consistent recovery rate – a testament to our global effectiveness. 4.97/5 Average rating from a diverse global clientele of over 5,000.

Register for a free profile and effortlessly upload your claim within just 2 minutes. We match your request with our expansive network of over 500 attorneys and collection firms to get you started quickly.

Access competitive legal action rates worldwide through our network of 500+ local attorneys. For legal interventions (lawsuits, debt enforcement, insolvency proceedings, etc.), receive up to 3 competitive quotes from our network of local attorneys.

Consolidate all your cases worldwide in one platform. Enjoy seamless case upload, management, and reporting. Upload cases manually, via CSV files, or utilize our REST API for custom integrations with full technical support from our developers.

What are the Advantages of Sending a Collection Letter?

Now that we've got the nitty-gritty costs out of the way, let's chat about the silver lining. Yes, my friend, sending a collection letter has its perks. From getting back the money you're owed to saving face with your clients, this little piece of paper (or email) can work wonders. Let’s break it down:

- Debt Recovery – The Main Event: Let’s be real, the primary goal of sending a collection letter is to get that dough back in your pocket. When invoices are gathering dust and polite reminders are getting ghosted, a collection letter is like your business’s superhero – swooping in to save the day (and your cash flow).

- Maintaining Professional Relationships – Keep It Classy: A collection letter doesn't have to be the bad guy. Crafted thoughtfully, it can actually help preserve that oh-so-valuable relationship with your client. It’s like saying, “Hey, we value your business, but we’ve got bills to pay too.” It’s a respectful way of handling a touchy situation, and it can leave the door open for future business. Because who knows? Today’s debtor could be tomorrow’s big spender.

- A Formal Record – Cover Your Bases: There’s an old saying – “The faintest ink is more powerful than the strongest memory.” Having a formal collection letter serves as solid evidence that you tried to collect the debt amicably. If things go south and you end up knocking on the courtroom door, this letter could be the ace up your sleeve, proving that you made a good faith effort to resolve the issue.

- Saving Legal Costs – A Stitch in Time Saves Nine: Speaking of courtrooms, legal battles are not just stressful – they’re pricey. Sometimes, sending a well-worded collection letter can nudge the debtor into action without escalating things into a legal tussle. And trust me, avoiding legal fees is like finding money in the pocket of an old pair of jeans – an unexpected and welcome surprise.

So, there you have it – a collection letter is not just about recovering debts; it's also about keeping relationships intact, having a paper trail, and potentially saving you a ton on legal costs. It's like a Swiss Army Knife for your business!

With all these perks in mind, you’re probably raring to get started. But what should you actually put in this wonder-letter? In the next section, we’ll discuss the key elements you should include in your collection letter. Stay tuned!

What are the Key Elements to Include in a Collection Letter?

Alright, let's get down to the nitty-gritty of what makes a collection letter effective. Just like a recipe needs its ingredients, a collection letter needs its key elements. These elements work together to create a persuasive and impactful message. Here's what you need to include:

- Debtor Information – Know Your Target: Start by addressing the letter to the debtor personally. Use their name and include their contact information, such as their address and phone number. This shows that you’ve done your homework and adds a personal touch to your letter.

- Amount Owed – Get to the Point: Be crystal clear about how much moolah is owed. Specify the exact amount, including any interest or late fees that may have accrued. Leave no room for confusion or ambiguity. The debtor needs to know the score.

- Due Date – Time Is of the Essence: Highlight the due date prominently. Make it clear that the payment was expected by a specific deadline. This helps create a sense of urgency and emphasizes the importance of settling the debt promptly.

- Payment Methods – Make It Convenient: Provide clear instructions on how the debtor can make the payment. Include multiple payment options, such as online platforms, checks, or bank transfers. The easier it is for the debtor to pay, the more likely they'll follow through.

- Professional and Empathetic Tone – The Magic Combination: Maintain a professional tone throughout the letter. Be firm, but never rude or disrespectful. Remember, you want to preserve the business relationship, even as you pursue the debt. Adding a touch of empathy can also go a long way in creating understanding and cooperation.

- Clear Call to Action – Tell Them What to Do: Don't leave the debtor hanging. Clearly state what you expect from them. Whether it's paying the full amount, setting up a payment plan, or contacting your accounts department, provide specific instructions. A call to action leaves no room for ambiguity and encourages a prompt response.

- Relevant Account Information – Cross the T's and Dot the I's: Include the debtor's account information, such as invoice numbers or reference codes. This helps both parties easily track and identify the debt in question. It adds credibility and ensures that there are no misunderstandings about the specifics of the debt.

Remember, each element serves a purpose. They work together to convey a concise and persuasive message. So, mix these ingredients wisely to create a collection letter that leaves no doubt about your expectations.

In the next section, we'll walk you through the step-by-step process of writing a collection letter. Stay with us!

How to Write an Effective Collection Letter: A Step-by-Step Guide

Writing an effective collection letter is a crucial step in recovering outstanding debts. Follow this step-by-step guide to craft a persuasive collection letter that increases your chances of successful debt collection:

- Gather the Necessary Information: Before you start writing, gather all the relevant information about the debt and the debtor. This includes details such as the debtor's contact information, outstanding amount, invoice numbers, and the due date. Having these details at hand will ensure accuracy in your collection letter.

- Set the Right Tone: Choose a professional and empathetic tone for your collection letter. While it's important to assert your rights, maintaining a respectful and understanding approach can help preserve the business relationship with the debtor. Strike a balance between firmness and empathy to convey your expectations effectively.

- State the Purpose Clearly: Begin your collection letter by clearly stating the purpose of the letter: to request payment for the outstanding debt. Clearly mention the amount owed, the due date, and any late fees or interest that have accrued. This sets a clear expectation for the debtor.

- Provide Relevant Details: Include all the relevant details related to the debt, such as the invoice numbers, services or products provided, and the original agreement terms. This helps the debtor easily identify the specific debt in question and minimizes confusion or disputes.

- Emphasize the Consequences of Non-Payment: While maintaining a professional tone, clearly communicate the consequences of non-payment. Explain that failure to resolve the debt may result in further action, such as involving a collection agency or pursuing legal remedies. This communicates the seriousness of the situation and encourages the debtor to take prompt action.

- Offer Payment Solutions, if Appropriate: If the debtor is facing financial difficulties, consider offering payment solutions. This could include proposing a payment plan or suggesting alternative methods of payment. Being flexible and accommodating can increase the chances of debt resolution.

- Provide Clear Instructions and Contact Information: Ensure that your collection letter includes clear instructions on how the debtor can make the payment. Include multiple payment options, such as online payment portals, mailing addresses, or contact details for your accounts department. Make it as convenient as possible for the debtor to fulfill their payment obligations.

- Proofread and Edit: Before sending your collection letter, thoroughly proofread and edit it for clarity, grammar, and spelling errors. A well-written and error-free letter enhances your professionalism and credibility. Consider having someone else review the letter for an additional perspective.

- Keep Records and Follow-Up: Maintain meticulous records of all communication and actions related to the collection process. Keep copies of the collection letter, any responses received, and notes of any phone calls or meetings. This documentation is essential if further action, such as involving a collection agency or pursuing legal options, becomes necessary.

By following these steps, you can create a well-crafted collection letter that maximizes the chances of debt recovery.

What to do After the Collection Letter Has Been Sent?

Congratulations! You've sent out your collection letter, but the journey doesn't end there. Now, let's talk about what to do next and how to handle different scenarios that may arise:

Possible Responses and How to Handle Each

- Payment: The ideal scenario! If the debtor responds by making the payment in full or in part, promptly acknowledge their payment and express appreciation for resolving the matter. Make sure to update your records accordingly and provide a receipt if necessary.

- Negotiation: Sometimes, the debtor may respond with a proposal to negotiate the payment terms or request a payment plan. Assess the feasibility of their proposal and consider the potential benefits of reaching a mutually agreeable arrangement. Engage in open and constructive communication to find a solution that works for both parties.

- No Response: Unfortunately, silence can be a common response. If you don't receive any response after a reasonable period, follow up with a polite reminder. It's possible that the initial letter was missed or overlooked. Persistence can pay off, and a gentle nudge might prompt the debtor to take action.

Escalating the Situation if No Response or Payment is Received

If the debtor continues to disregard your collection efforts, it may be necessary to escalate the situation. Determine the threshold at which you're willing to pursue further action. This could involve engaging a collection agency, initiating legal proceedings, or seeking the advice of an attorney.

Documenting the Process for Potential Legal Proceedings

In case legal action becomes necessary, it's crucial to document the entire collection process. Maintain a comprehensive record of all communication, including copies of the collection letters, receipts, emails, and any other relevant documentation. This documentation serves as evidence of your attempts to resolve the debt and can support your case if it comes to legal proceedings.

Be diligent in organizing and storing this information securely. It's always better to be over-prepared than under-prepared in legal matters.

Remember, each response or lack thereof requires careful consideration and appropriate action. Maintain professionalism throughout the process, even if tensions rise. Communication and persistence are key to finding a resolution.

Free template

.webp)